Quick Answer

The best bank card for children and teenagers depends on their age and your family’s needs. For children under 12, dedicated children’s banking apps like GoHenry, HyperJar Kids, or Rooster Money offer parental controls and spending limits. For teenagers aged 11-17, many high street banks including Starling Bank, Monzo, Lloyds, and NatWest provide current accounts with contactless debit cards. Most accounts are free, though some specialist services charge monthly fees of around £2-£4.

Introduction

If you’re a parent in the UK, you’ve probably faced the question: when should your child get their own bank card? Whether it’s for managing pocket money, paying for school trips, or teaching financial responsibility, choosing the right account can feel overwhelming. With options ranging from prepaid debit cards for kids to full bank accounts for teenagers, the landscape has changed dramatically over the past five years.

The Financial Conduct Authority (FCA) regulates all these products to ensure consumer protection, but not all children’s accounts are created equal. According to MoneyHelper, more than 1.5 million children in the UK now have some form of bank account before their 16th birthday, reflecting a growing trend towards early financial education. This guide cuts through the confusion, covering everything from GoHenry alternatives to Monzo teenager accounts, so you can make an informed decision for your family.

Key Takeaways

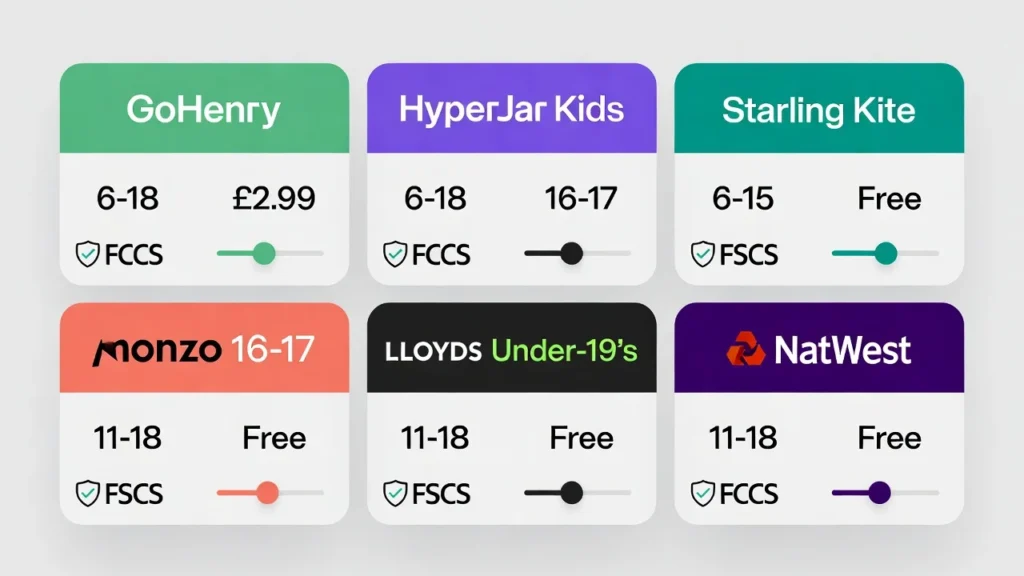

- Age matters: Most children can get a prepaid card from age 6, but bank accounts typically start at age 11

- Free options exist: High street banks like Lloyds and Starling offer free children’s accounts with no monthly fees

- Specialist apps charge fees: GoHenry and similar services cost £2-£4 monthly but offer more granular parental controls

- No ID required? Some prepaid cards have lighter ID requirements, but bank accounts always need proof of identity

- Teenagers can access advanced features: Older teens may get overdrafts, savings pots, and international spending options

What Are Bank Cards for Under-18s? A UK Guide for Beginners

A bank card for under-18s is either a prepaid debit card or a standard current account debit card designed specifically for children and teenagers. Unlike adult accounts, these come with built-in parental controls, spending limits, and educational tools to help young people learn money management.

In the UK, these products fall into two main categories:

- Prepaid cards for kids: Brands like GoHenry, HyperJar Kids, and Rooster Money operate as electronic money institutions (EMIs) regulated by the FCA. Your child gets a card linked to a parent-controlled account. You load money, set limits, and monitor spending via an app.

- Children’s current accounts: Banks like Starling Bank (Starling Kite), Monzo (for 16-17 year olds), Lloyds, NatWest, and Bank of Scotland offer proper bank accounts with debit cards. These are full bank accounts, meaning your money is FSCS protected up to £85,000.

The key difference lies in regulatory protection and age restrictions. Prepaid cards typically accept children from age 6, while current accounts start at age 11.

How Bank Cards for Under-18s Work in the UK

Getting a bank card for your child involves a straightforward process, though requirements vary by provider. Here’s how it typically works:

1. Choose your provider

Decide between a prepaid card specialist (GoHenry, HyperJar) or a traditional bank account (Starling, Lloyds, NatWest). Consider monthly fees, age requirements, and features.

2. Verify your identity

As the parent or guardian, you’ll need to provide proof of identity and address. For the child, a birth certificate or passport is usually required for bank accounts. Some prepaid cards accept lighter verification.

3. Set up parental controls

Once approved, you’ll download the provider’s app. You can set daily spending limits, decide where the card works (online, in-store, ATM), and receive notifications for every transaction.

4. Load money onto the account

For prepaid cards, you transfer funds from your own bank account. For children’s current accounts, you can set up standing orders for pocket money.

5. Activate the card

The card arrives by post. Most providers require activation via the app or website. Cards are typically contactless, with Apple Pay and Google Pay available on many accounts.

6. Monitor and adjust

Use the app to review spending, add money, and gradually increase limits as your child demonstrates responsible use.

7. Transition to an adult account

Most children’s accounts automatically convert to standard accounts at age 18, or you can switch to a student account if your child goes to university.

Takeaway: The process takes about 5-10 minutes for prepaid cards and up to 5 working days for traditional bank accounts to verify documents.

Real UK Examples & Scenarios

| Scenario | Situation | Outcome | Key Lesson |

|---|---|---|---|

| Manchester family with 8-year-old | Parents want to teach pocket money management with controlled spending. | Choose GoHenry for £2.99/month. Child gets card with £10 weekly limit, parents set chores in app. | Prepaid cards work well for young children where bank accounts aren’t available. |

| Glasgow teenager aged 16 | Needs a debit card for part-time job wages and school expenses. | Opens Starling Bank account (Starling Kite). Gets full UK sort code, account number, contactless card, and can use Apple Pay. | A real bank account builds credit history and offers full banking features. |

| Bristol parent with multiple children | Wants a free solution for three children aged 11, 13, and 15. | Uses HyperJar Kids free version with one parent account linked to multiple child accounts. | Free alternatives exist but may have fewer features than paid services. |

Pros and Cons of Bank Cards for Under-18s

| Pros | Cons |

|---|---|

| Teaches financial responsibility with real-world spending experience | Monthly fees for prepaid cards can add up over time (£36-£48 annually) |

| Parental controls allow instant spending limits and transaction monitoring | Bank accounts for under-16s often have no overdraft or credit-building features |

| Cards are contactless and work with Apple Pay/Google Pay | Some providers require a minimum top-up or charge for replacements |

| FSCS protection on bank accounts up to £85,000 | Prepaid cards may not offer FSCS protection (though funds are safeguarded separately) |

| Reduces need for cash and teaches digital money management | Children can still overspend if limits aren’t set carefully |

Key Factors That Affect Children’s Bank Cards in the UK

Age Requirements

Most prepaid cards start at age 6, while bank accounts typically require the child to be at least 11. Some accounts like Monzo teenager account only open from age 16.

Parental Consent and Verification

UK law requires parental consent for under-18s. You’ll need to prove your identity and relationship to the child. Proof of address (utility bill, council tax) and child’s birth certificate are standard requirements.

FSCS Protection

Funds in a bank account are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000. Prepaid cards hold money in safeguarded accounts, offering protection but not FSCS coverage.

Spending Controls

Look for real-time notifications, merchant blocking, and ATM limits. Some providers let you block specific categories like gambling or online spending.

Account Transition

Consider whether the provider offers a seamless transition to an adult account at age 18, or if you’ll need to close and reopen elsewhere.

Fees and Charges

Check for monthly fees, card replacement costs, ATM withdrawal fees, and foreign transaction charges. Some children’s accounts charge for spending abroad.

International Use

If your child travels, check if the card works abroad. Starling Bank and Monzo offer fee-free spending overseas, while prepaid cards may charge.

Common Mistakes UK Consumers Make

Choosing the wrong type for the child’s age

Many parents try to open a bank account for a 7-year-old, only to be rejected. Check age limits before applying—prepaid cards are the only option for younger children.

Ignoring fees on prepaid cards

£2.99 a month might seem small, but over five years that’s nearly £180 per child. For multiple children, a free alternative like HyperJar Kids or a bank account could save significantly.

Forgetting to update ID

If your child’s passport or birth certificate is outdated, applications can be delayed. Keep documents current before applying.

Overlooking FSCS protection

Some parents assume all children’s cards have the same protection. Bank accounts offer FSCS protection; prepaid cards do not, though funds are safeguarded.

Setting limits too high

Giving a teenager a £500 limit without guidance can lead to overspending. Start low and increase as your child demonstrates responsible use.

Not checking ATM withdrawal limits

Some children’s accounts have strict ATM limits (e.g., £50 per day). If your child needs cash for a school trip, ensure the limit meets their needs.

Expert Insight

“Financial education starts early. The FCA encourages parents to involve children in money management from a young age. Using a prepaid card or children’s account with parental controls is one of the most effective ways to teach budgeting skills in a safe environment. However, always check that the provider is authorised—you can verify this on the FCA Register.”

— Financial Conduct Authority (FCA), Consumer Warning Notice

Is a Children’s Bank Card Worth It for UK Users?

For most families, a dedicated children’s card is absolutely worthwhile—but the right choice depends on your circumstances.

Who should consider it:

- Parents with children aged 6-10 who want a controlled introduction to money

- Teenagers with part-time jobs needing a place to receive wages

- Families wanting to reduce cash and simplify pocket money management

- Parents preparing children for university or independence

Who should NOT consider it:

- Families who prefer cash-based pocket money with no digital tracking

- Parents concerned about monthly fees and willing to wait until age 11 for a free bank account

- Children who already demonstrate poor financial judgement and need stricter supervision

Alternatives to consider:

- Cash in a piggy bank: Traditional but lacks educational features

- Savings accounts: Better for long-term saving, not everyday spending

- Parent’s card with strict rules: Free but offers no independent learning

If you’re unsure, consult MoneyHelper or a qualified independent financial adviser, especially if you’re managing complex family finances or have concerns about your child’s spending habits.

UK Regulatory Information

Children’s bank cards and accounts in the UK are regulated by the Financial Conduct Authority (FCA) . All providers must be authorised and appear on the FCA Register.

- FSCS protection applies to deposits in authorised banks up to £85,000 per person, per institution. This covers children’s current accounts from banks like Lloyds, NatWest, Starling, and Monzo.

- Prepaid card providers are typically authorised as electronic money institutions (EMIs) . While they must safeguard customer funds, these funds are not covered by FSCS.

- Consumer protection rights under the Consumer Rights Act 2015 apply to all financial services. You have the right to complain to the Financial Ombudsman Service if you’re unhappy with how a provider handles your issue.

- MoneyHelper (formerly Money Advice Service) provides free, impartial guidance on children’s accounts and financial education.

To verify a provider’s authorisation, visit fca.org.uk/register or contact MoneyHelper for guidance.

Conclusion & Next Steps

Choosing the right bank card for your child comes down to three key considerations: age, cost, and features. For children under 11, prepaid cards like GoHenry, HyperJar Kids, or Rooster Money offer the best combination of safety and parental oversight. For teenagers, a free bank account from Starling, Monzo, Lloyds, or NatWest provides real banking experience without monthly fees.

Your next steps:

- Assess your child’s age and maturity level to determine the appropriate type of account.

- Compare costs—calculate total fees over the time your child will use the account.

- Check eligibility by reviewing the provider’s ID requirements and application process.

- Set up parental controls from day one, starting with low limits and increasing gradually.

- Review regularly—use the app to monitor spending and adjust as your child grows.

For more information, visit MoneyHelper.org.uk for free guidance, or check the FCA Register to verify any provider you’re considering.

Frequently asked questions UK families guide

You must be 18 years old to get a credit card in the UK. Under-18s cannot legally enter into a credit agreement. However, children can have debit cards linked to current accounts or prepaid cards from age 6.

Yes, HyperJar Kids offers a free version with one parent account and multiple child cards. Rooster Money also has a free basic plan. However, free options often have limited features compared to paid services like GoHenry.

Yes, many banks offer children’s savings accounts from birth, but these are savings accounts, not current accounts with debit cards. For a debit card, you’ll typically need to wait until the child is at least 6 (prepaid) or 11 (current account).

GoHenry is a prepaid card with a monthly fee, aimed at younger children (age 6+), with extensive parental controls. Starling Kite is a free bank account for children aged 6-15, linked to a parent’s Starling account, offering FSCS protection and no monthly fees.

For Monzo accounts, UK cash withdrawals are free up to £250 per month, then 3% fee applies. For Monzo teenager accounts (age 16-17), the same limits apply. Always check the latest fee schedule in the app.

If you’re using Monzo’s 16-17 account, you can transfer money directly from your own Monzo account or any UK bank account using the sort code and account number. For younger children, Monzo doesn’t currently offer dedicated child accounts.

A PPC (Prepaid Prescription Certificate) is separate from children’s banking. It’s a certificate from the NHS that allows unlimited prescriptions for a fixed cost. This is not related to bank cards but appears in related searches.